Jump to:

Introduction

Intertek Plc overview

Quality of Intertek

The dividend question

Financial health

Growth

Acquisitions

So, is Intertek a great company?

Valuation

Conclusion

Summary of Study

- Intertek is a good company e.g. it has good CROCI – cash return on capital invested, a respectable operating margin, and a decent track record of these metrics.

- It has excellent dividend track record, growth, cover and consistency.

- However, it isn’t all a rosy picture and there is room for improvement e.g. overcoming the annual impairments/exceptionals.

- It is currently being sold at a good price.

Introduction

AziziFund’s method of investing is simple and not unique; we

aim to buy the world’s greatest companies at attractive prices and hold for the

long-run to realise the compounding of cash profits. I want to share with the

reader and existing investors our research on the FTSE 100 listed company Intertek Plc

to see whether it fits this investing objective. The conclusion is: a

‘cautionary yes’, but read on to find out more.

Firstly, let's talk about the company

Intertek tracks its history to over 130 years ago. It began by

providing independent testing and certification of ship’s cargos [see here].

Over the many years, it has acquired new businesses and has become a

significantly larger and a more evolved company. Today, Intertek is a company

with many services and to get one’s head around everything it does is not easy.

I’ll make an attempt at communicating their activities briefly, but I would

refer you to the company website, which is incidentally quite informative, to

better understand everything it does.

In brief, Intertek divides all of its services into 4 categories:

In brief, Intertek divides all of its services into 4 categories:

- Testing

- Inspection

- Certification, and

- Assurance

For example, within Testing, it provides

automotive testing, chemical testing, food testing and (I count) 18 other

testing services. Within Assurance, it provides Management Systems

Certification, Supply Chain Assessment, Benchmarking in Quality &

Performance etc. So each of these four categories have sub-categories. I am

nervous to cite any specific example of their services as I think it risks

underestimating the scope of their work. So again, I refer the reader to the

company’s website for the details.

Moreover, it provides these services to all sorts of industries e.g. chemical, construction and engineering, energy & commodities, food & healthcare etc. globally in over 100 countries.

I think suffice to say Intertek works with all sorts of companies in many industries and all around the world. So, in essence it is a highly diversified company. The strength here is that it is not dependent on any particular company, country or service. Of course, the potential concern for a super-diversified company is reduced operating margins due to lack of focus – more on this later. Amongst the characteristics I also look for a company is whether its products and services are compelling enough to be needed in all business economic conditions i.e. it’s not particularly cyclical and so economic recessions do not acutely hurt hit. It is not very easy to give a view about this just on the basis of the services it provides, but I think looking at the historic numbers over the economic cycle should be a good and reliable indicator, again, more on this later.

Moreover, it provides these services to all sorts of industries e.g. chemical, construction and engineering, energy & commodities, food & healthcare etc. globally in over 100 countries.

I think suffice to say Intertek works with all sorts of companies in many industries and all around the world. So, in essence it is a highly diversified company. The strength here is that it is not dependent on any particular company, country or service. Of course, the potential concern for a super-diversified company is reduced operating margins due to lack of focus – more on this later. Amongst the characteristics I also look for a company is whether its products and services are compelling enough to be needed in all business economic conditions i.e. it’s not particularly cyclical and so economic recessions do not acutely hurt hit. It is not very easy to give a view about this just on the basis of the services it provides, but I think looking at the historic numbers over the economic cycle should be a good and reliable indicator, again, more on this later.

Is Intertek a great company?

Let us begin by looking at the company’s historic operating

profits from 2007 – before the recession occurred:

My thoughts on this chart are:

- The general trend of profit rise is good and encouraging.

- The large loss of £283 m recorded in 2015 is very disappointing as it ruins the good track record, and begins to invoke scepticism about consistency. NB: the total impairment was actually £626.9 m and it was related to Industry Services.

- Exceptionals and/or impairment are being recorded almost every year over the past 11 years and the gap between recorded and normalised (or adjusted) figures are not so insignificant so as to be ignored. This adds to my initial sense of scepticism.

So, when it comes to profitability, it is mostly good

but has does have a problem.

With respect to the company’s efficiency in making money, which can be calculated by its return on capital employed (ROCE), or adjusting for leases which would be more representative i.e. lease-adjusted ROCE, see the graph overleaf.

Looking at the graph:

With respect to the company’s efficiency in making money, which can be calculated by its return on capital employed (ROCE), or adjusting for leases which would be more representative i.e. lease-adjusted ROCE, see the graph overleaf.

Looking at the graph:

- Based on the latest full year number (2017), I compute the company’s lease-adjusted ROCE is circa 24% which is very good.

- You can see that the historical trend is fairly consistent and it has always been above 17% which is still quite good. There was a small downturn from 2010 to 2014, but the situation has materially improved since 2014.

The operating margins have improved a little from c.16% in

2008 to c.18% in 2010 and has stayed fairly consistent since then.

Therefore, all decreases and increases to the ROCE has been

driven purely by the capital turnover (sales over capital employed), e.g. for

every £1 in invested, it was able to make sales of more than £1.3 in 2017. The

situation in 2014 was comparatively worse because the sales for that year were

lower although the capital employed had been at its historical highs.

The situation improved in 2015 because the capital employed

were reduced (an impairment charge meant writing off some of the assets which I

talked about already) whilst sales had increased. Since 2015, the improved ROCE

has continued to improve mainly from increased sales and small contribution

from a reduced capital employed, which is good.

Overall, I would say this graph says that Intertek has the

key sign of a quality business; a high ROCE with a decent track record.

There are a number of other metrics I look at when assessing

quality of a business; cash returns on capital invested (CROCI), cash

conversion (percentage of profits which are actually cash) and capex ratio (the

proportion of operating cash flow spent on capex). Here is a summary table:

So, we can see that:

So, we can see that:

- CROCI is generally good although in 2013 and 2012 it did drop below 10% (which is the level below which I tend to avoid companies). The reason here is again higher capital employed in comparison with the achieved free cash flow (FCF). However, the situation has been improving radically since then which is good.

- Profits are converted into decent cash for many years, although in the years 2011, 2012 and 2013, the numbers were disappointing since the conversion rate was below 80%. Again, there is a consistency issue with this company.

- Capex ratio over the past 2 years was c. 25% on average which is mediocre, i.e. it needs to spend about 25% of its operating cash flows on Capex to stay in business. However, there have been many years where it was well above 30% which means this is a somewhat capital-intensive business. This is a very strange feature of Intertek because the description of this business would not normally be associated with capital intensive activity. I’ve checked the depreciation and amortisation (D&A) cost and compared it to the capital expenditure (Capex), and the is Capex is generally just about covering the D&A. This means the D&A is usually high for such a business and perhaps something to further investigate.

What about the dividend?

Here is the beautiful picture over the past 11 years:

- Dividends have been continuously paid over the past 11 years and have been growing which is fantastic.

- FCF dividend cover has always been good or decent (i.e. 2012/13), which means dividends should continue to grow and be paid from the FCF. Again, this is very good.

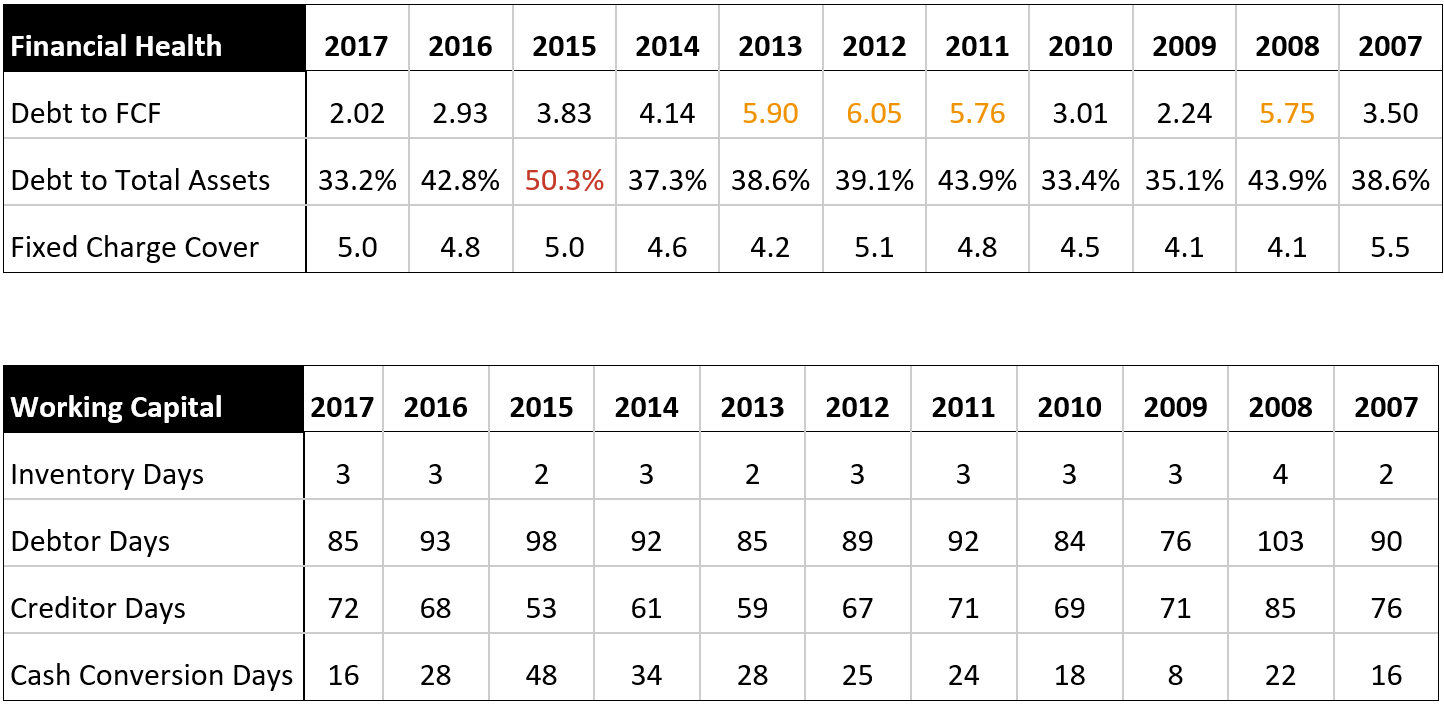

Financial Health?

Here is another graph and a few tables of the situation for the past 11 years:

What does these mean?

- Its total debt is not small, but the fixed charge cover (i.e. how many times over the profits can service the debt and pay for operating leases) and debt/FCF look okay which means the situation is acceptable although not necessarily fantastic

- Historically, there has been one time where the debt/assets was more than 50% which is a little concerning. The company seems to need to borrow a lot of money to do its operation which is not the ideal company in my view.

- The pension deficit is very small and not a problem.

- The working capital cycle is quite low as indicated by the cash conversion days so there should not be any liquidity problems at all. For example in 2017, the number of days between the time cash left the business for its operation and when profits came back into the business was 16 days, which is very small and therefore great. Moreover, the cash conversion days has been improving over the past few years which is also good i.e. the business is becoming more effective in managing its working capital which in this case is due to reduction in debtors.

Growth

Well, there are many metrics we can measure that by, so here is a summary:

I always look at compounded growth numbers because year to year changes can be very misleading; Benjamin Graham gave warnings of this in his books.

- The company's long-term growth rate (e.g. 10 years) has been very good in all metrics:

o 10-year CAGR of sale has been 13.6%,

o 10-year CAGR of FCF/share has been 17.2%, and

- In the shorter 5-year periods, the growth has also been quite good in recent years – see the table above.

Other Matters

I haven’t shown the data for the following comments to keep

the article brief, but the diligent investor may want to know the conclusion to

a number of other matters as follows

- The company only mildly benefits (and suffers) from operational gearing i.e. percentage increase in sales has a multiplier percentage increase in profits. There are a few years e.g. in 2017 where the picture is a little inconsistent.

- Share dilution (i.e. issuing new shares) is occurring but not on a massive scale e.g. between 2007 and 2017 (11-year period), the shares on issue increased by c. 3%.

Acquisitions

One of the main characteristics of Intertek that stands out to me is the constant acquisition. This normally makes me quite nervous as the profitability numbers (e.g. EBIT margin, ROCE etc.) usually take a hit as companies tend to overpay. Worst still, an impairment can be recorded when the acquisition doesn’t work out and so all the cash invested goes to waste which basically means destruction of share-holder value.

The table below summarises all the acquisitions of Intertek

since 2007:

The total spend on acquisitions over the past 11 years

has been c. £1.2 billion, whilst the total FCF generated over the same period

was c.£1.8 billion. So the company has spent c. 66% of its FCF over the past 11

years on acquisitions and this is a huge number. It seems acquisitions have

become part of the DNA of Intertek. I think this point can give some meaningful

insight into Intertek:

·

The large portfolio of its

services is due to the many acquisitions it makes i.e. Intertek effectively

bolts-on new businesses as opposed to making them from scratch.

·

The growth in sales and

profits has probably come from acquisition.

·

The significant debt is

probably due to the acquisitions.

There is an issue with this way of running a business;

acquisitions are not a long-term sustainable way of growing a business. It also

runs the risks of acquisitions going sour and destroying shareholder value.

Indeed my fears of impairments are true for Intertek; almost

every year Intertek records exceptionals (or non-recurring losses) and in 2015

there was a large impairment recorded against one of its businesses. This is

disappointing.

With respect to whether the profitability of the company has

been dented, actually ROCE has been generally quite good, which means that

acquisitions have not been ridiculously expensive which is good.

In an ideal world as a shareholder, I would like the company

to first focus on its existing assets and portfolio of services; they should

try and improve the quality of their services and hopefully be able to command

either greater margin or at least get more sales which will feed into higher

ROCE. Once this project has been comprehensively executed and the gains have

been saturated, I don’t mind careful and inexpensive acquisitions.

I’ve read through the company’s strategy and I’m afraid to

say that we will see more acquisitions, and so probably we will see more

exceptionals and impairments recorded in the future. Perhaps the saving grace

is the company is at least aware of acquiring “high-margin and high-growth”

[see here]

opportunities.

Conclusion on whether Intertek a great company?

There are lots of good things about Intertek:

·

Good CROCI, a respectable

operating margin, and a decent track record of these metrics.

·

Decent cash conversion for

most years.

·

A very diversified

portfolio of services in all parts of the world. The sales and profitability

numbers in 2008/09 tells me that Intertek is not a cyclical company i.e. it does

well in recessions which is great.

·

Excellent dividend track

record, growth, cover and consistency.

·

Very good and consistent

growth in sales and FCF.

Having said this the company also has the following

problems:

·

Constant

impairments/exceptionals recorded almost every single year for the past 11

years.

·

Some inconsistency in

achieving high ROCE and CROCI i.e. it was lower than desired for a few years.

·

Cash conversion for a

number of years (2011, 2012 and 2013) was disappointing.

·

Capex ratio for many years has

been above 30% which is not ideal (i.e. there seems to be a fairly intensive need

to spend to stay in business) and very strange for such a company.

Although overall, none of these problems are

insurmountable and they don’t render the good attributes of the company void.

So, in my opinion, Intertek is right now a good company although not (yet) a

great company. There is room for improvements, and there are various aspects

which the investor needs to keep an eye on e.g. future acquisitions, financial

health, ROCE, cash conversion, capex ratio etc.

Valuation

My method of valuation is very simple and not unique; I

compare the cash returns for the price I have to pay to buy the company outright

i.e. just like the cash yield I get if I was to buy a house to rent out. I

judge whether this cash yield is satisfactory against other investment

opportunities available to me. If the cash yield is better than other

investment opportunities, it is good value. If the cash yield is below what

other investment opportunities offer, I would then estimate a future growth

rate of the company’s cash profits per share to see how long I have to wait

before I get my desired yield, and I ask myself whether I’m willing to wait

that long. If it is too long, I am afraid the company is too expensive for my

liking.

So technically there are three components to the valuation

process I describe:

1.

The company’s cash profits;

I would typically use the company’s latest FCF which for Intertek was £319.7

million in 2017. However in 2017, Intertek’s working capital was at the lower

end of its historical norms; the debtors dropped (i.e. the company was owed

less from its customers than is customary) which gave a small boost to FCF.

This means the FCF is abnormally higher than would be sustainable in my opinion

and so we have to careful about using the latest FCF for this calculation. In

this situation I would calculate the estimated cash profits (basically

Warren Buffet’s method of working out the cash profits - see here for more details) of the company. For

Intertek in 2017, I estimate the cash profits to be £311.5 m (NB: this is

slightly lower than the FCF in 2017 as I expected for reason I gave above). We

can divide this by the company’s market cap to obtain the cash yield.

The current share price of Intertek (at the time of

writing this article) is c. £46 per share, or a market cap (the price for the

company) of £7.3 billion. The cash yield is: £311.5 m / £7.3 b = 4.3%.

2.

With respect to whether

this achieved cash yield is satisfactory, we have to compare this to other

investment opportunities, or a reduced-risk rate (also known as a risk-free

rate). My provisional and estimated answer is 5.4%.

You may be wondering ‘What? How? Why?’

Well, that would be the subject of another article so

all I would say right now is: this figure is simply the UK’s current inflation

rate (sitting at 2.4%) plus an interest rate which I arbitrary choose to be 3%.

This 3% is simply what I opine to be a more ordinary interest rate than what

we’ve been having over the past 10 years. NB: The gilt rates are abnormally low

so they should be ignored. As a side point, some houses in the north of UK can

give you rental yields higher than 4.3%.

Note that the achieved cash yield is lower than the

reduced risk rate (i.e. 5.4%) which is not ideal. So why should you buy

Intertek when there is better value elsewhere? Read on…

3.

The growth rate of FCF.

Looking at the table showing the various growth metrics, I would estimate that

an annual growth rate of 15% for the FCF seems reasonable.

With an annual growth rate of 15%, you only have to

wait 1.5 years (actually only 1 year since we have already had 6 months of

operation) to get to the target reduced risk yield. The house rental yield and

the long-term house-price appreciation combined do not have a 15% annual growth

rate. This is the reason Intertek is a better investment proposition than

buying a house to rent out. You just have to stomach the share price

volatility!

If you are willing to wait one year to get this yield,

which I think you should since one year for a long term investor is trivial,

Intertek is currently being sold at a fair price. I personally also like to

compare the valuation of a company against its own historical norms. This tells

me something about how the market has viewed it historically. Such a graph can

perhaps be used a cautionary indicator of what the future valuation might look

like.

As you can see from the graph below, a current yield of

4.3% is not the cheapest or most expensive price Intertek has seen. This tells

me the current 4.3% yield is nothing to worry about.

I should reassure the reader that the half year 2018

results are currently out, and it looks decent.

Conclusion

From the perspective of an investor, there is room for

improvement when it comes to Intertek e.g. more consistent and higher CROCI and

cash conversion. Nevertheless, Intertek still has many attributes of a good

company and is better than most companies in FTSE 100. Moreover, it is

currently sold at a decent price. Based on this, I would add Intertek as a

relatively small position in my portfolio. All the best to everyone investing!